“A lot of people with high IQ’s are terrible investors because they’ve got terrible temperaments. You need to keep raw irrational emotion under control.”

Charles Munger, Vice-Chairman of Berkshire Hathaway, is right. You could be the smartest person in the world, but you might end up being a self-destructive investor.

If you flash back to last week’s post, I talked about why dollar cost averaging was important, and how you’re able to take advantage of stock sales when the market is down. I also said that when you invest in the market monthly or periodically, you’re more likely to stick with investing. That all makes sense, right?

Prospective clients come into the office too many times with an account they’ve decided to manage themselves. If you’re an investor, you want what’s best for your account. Your emotions can get in the way of that though.

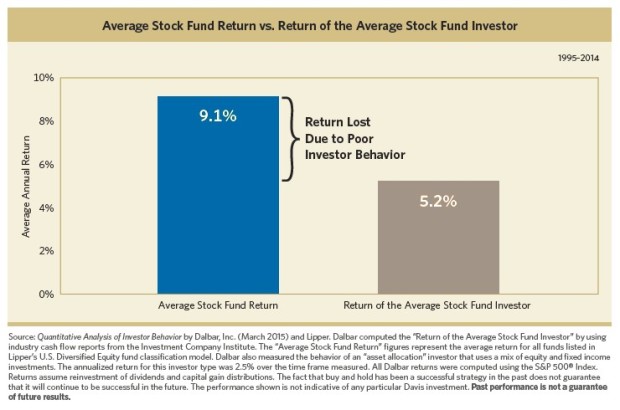

I saw this graph and wanted to share it with you. It compares the average stock fund return to the return of the average stock fund investor. The average stock fund investor is getting a 5.2% return annually. This might not seem bad, you might even be saying, “Well that’s a lot more than what my savings account earns.” You’re right! But that average stock fund investor missed out on an additional 3.9% return. I would be willing to bet that if they could go back and stick with a stock fund, and get that additional 3.9%, they would.

I think it’s safe to say we would all rather have a 9.1% annual return than a 5.2% annual return.

There are some skeptics out there, I’m sure. They think they’re great investors and they don’t fit into the chart. They think that they effectively time the market, and they can chase hot investments. They feel like they can do better by doing it themselves. This next paragraph is for the skeptics.

The market goes up and down. You know how you feel when that happens. For most investors, when the market makes a comeback from a low point, they start to get excited. They typically buy stocks or add money into stock funds. Things are looking up, and they’re investing in the market. The market keeps climbing and they’re thinking “Wow, I’m the smartest person in the world.” The market hits it’s peak. They’re ecstatic. Know what happens after something peaks? It starts to drop again. Now that investor has anxiety. Most of the time they’ll deny the drop, and the market keeps going down. They’re thinking “This was a horrible decision, I should get out before it bottoms out.” Enter panic mode. They sell. They say they’re never investing again. Market hits bottom and they think, “Good thing I got out when I did!” Do you know what happens next? The market makes a comeback. Now they’re upset. The market grinds higher and they want back in.

Do you see the problem here? When the typical investor feels excited about the market and thinks they’ve made the best decision ever, the market is getting to its peak. This is when investors have the most risk of loss. When the market is down and the investor is glad they got out before rock bottom, they missed out on the largest potential to earn.

This is why the average stock fund investor ends up doing worse than the average stock fund return. You should buy when the market is low, and sell when the market is high. Most investors do exactly the opposite.

Being an investor is hard. Your emotions can and most of the times will get the best of you. Having a plan and sticking to it is one of the most important things to do as an investor. If you make systematic investments, you are more likely to outperform the market. A financial advisor can help you stick to your plan when the market is fluctuating, reassure you when volatility is high, and help you stay disciplined and focused on your long term goals.

Instead of a sweet treat this week, I’m going to share a client story with you. With their permission of course.

Client XXX was getting ready for their first child. They knew how expensive college was and how important it was to have money set aside.

Their goal? Save for college. Their plan? $250 a month.

They opened a 529 account for their daughter and contributed $250 a month, every month, on the 20th. Baby number two came around not too long after and they put the same amount of money into another 529 on the same date of the month, every month.

The client contributed this way for eighteen and a half years per child. Let’s do the math together. 18.5 years times 12 months in a year times 250 dollars equals a grand total of $55,500 per account.

Do you want to know how much money they had in each 529 after eighteen and a half years? It was upwards of $300,000. By the time their children went to school, they didn’t care whether they went in state or out of state, and they didn’t have to worry about not having the resources to pay for it. Because they stuck to their plan, they were prepared for whatever might happen.

That is the power behind having a plan and sticking to it. When you make a plan to systematically invest and you don’t try to time the market on your own, odds are you will end up doing better than you otherwise would.

Don’t let your emotions get in the way of your investments. Need a plan or help sticking to it? You might want to consider a financial advisor.